Who Owns the AI Economy?

As AI shifts income from labor to capital, we need to rethink taxation and redistribution. A levy on large firms, paid in their own non-voting shares to a public benefit trust and enforced through market access, sidesteps the failures of past wealth taxes. The proceeds could be used to pay every citizen a dividend that scales with AI's advance. The international club that enforces the levy could also give AI governance a mechanism to temper the AI arms race.

Introduction

A PDF version of this post is available for printing.

When industrial machinery displaces an assembly line worker, or software displaces a call center worker, a part of their salary becomes income for the capital owner. Historically, this shift was tempered by two counterforces. Automation created new jobs that machines could not do, and human work became more specialized and better paid

As this trend continues, two problems arise. The immediate one is distributive: capital concentrates and compounds in the hands of the few.

The AI-safety literature has reached the distributive problem from its own direction: the "windfall clause" would have leading labs pre-commit a share of extreme profits to the public

The proposal below starts with a 1% floor aimed at the concentration and fiscal imbalance already present, and the rate rises only if labor’s share falls further. The fund would take decades to mature, so workers displaced early would still need separately financed transition support.

The tax system’s focus on labor income is not without reason: taxing capital correctly is hard. While taxes on income and realized gains from capital are administrable, the ability of taxpayers to defer realization, reinvest, and move capital across borders limits how much these taxes can raise. A natural next step is a wealth tax, which taxes the value of the capital directly, regardless of when it produces income or where that income is booked.

But three problems stand in the way

Recent U.S. proposals face the same problems. Warren's and Sanders's individual wealth taxes require the IRS to value every private business, piece of real estate, and art collection owned by anyone above the threshold, annually and under adversarial conditions. A cash obligation on illiquid wealth forces asset sales, and wealthy individuals can change their domicile (e.g., Facebook's co-founder Eduardo Saverin renounced U.S. citizenship before the company's IPO). Mark-to-market proposals (Wyden's Billionaires Income Tax, Biden's minimum tax on unrealized gains) are only slightly less impractical. While they avoid the deferral problem for publicly traded assets by taxing gains as they accrue, they still demand cash for paper gains, still struggle with assets that do not trade (valuing them each year or falling back to deferral charges), and still target individuals who can relocate.

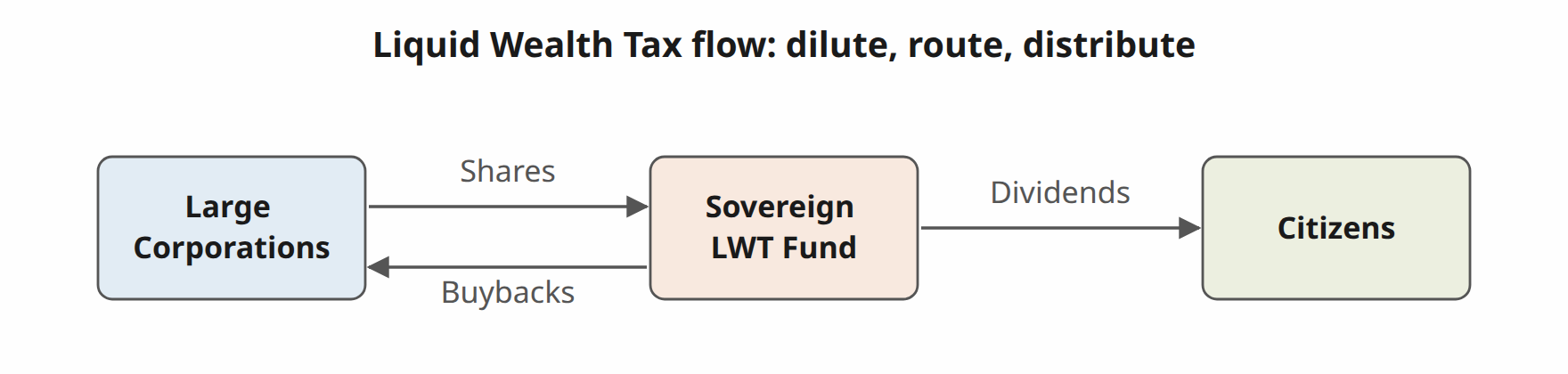

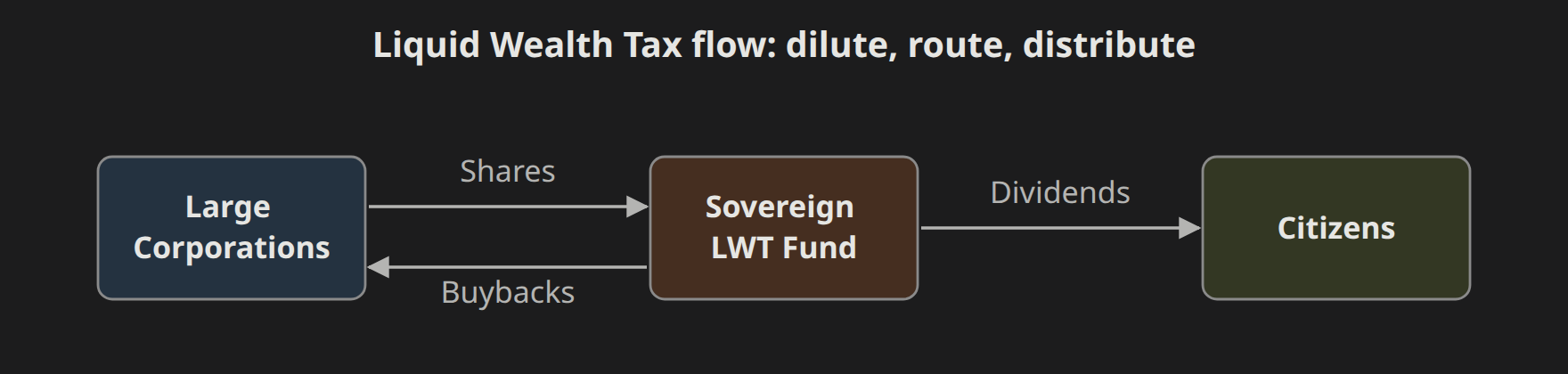

A liquid wealth tax

What if, instead of a cash tax on wealth, we required large corporations to pay a tax denominated in newly issued shares? On its face, such a tax would amount to a naturally progressive, valuation-free, indirect tax on individual wealth that defers the liquidity issue until later.

The idea is natural enough that multiple people I’ve spoken with have reinvented it with minimal prompting: forced sales for a cash tax would only crash the market, so tax the shares themselves. In the literature, Saez and Zucman worked out the economics of such a tax in a 2021 proposal

In the AI debate, Sam Altman's "American Equity Fund" is the closest of all to this post: a levy on large companies paid in their own shares into a fund that pays every citizen a dividend. Altman also considers avoidance, the treatment of private firms, dividend sizing, and a constitutional cap on the rate

A share tax largely sidesteps the valuation issue: 1% is 1% regardless of the company’s value.

The most plausible path for a liquid wealth tax is to structure it as a corporate excise on the privilege of doing business in corporate form, following Flint v. Stone Tracy Co. (1911), which upheld such an excise measured by income. Measuring it by equity value rather than income goes beyond Flint itself, but the underlying logic (taxing a corporate privilege, not property itself) is the same, and it has historical precedent: the federal capital-stock tax of 1916–1926 was a levy on doing business measured by the fair value of a corporation's capital stock, administered and litigated for a decade as a privilege excise without its constitutionality being drawn into question (Hecht v. Malley, 1924; Ray Consolidated Copper Co. v. United States, 1925). That measure was not simply the market value of the shares, though, and no court squarely passed on a capital-value measure under the direct-tax clause, so the precedent is supportive rather than settled. Most recently, Moore v. United States (2024) upheld a tax on a foreign corporation's realized but undistributed earnings, attributed to U.S. shareholders, while declining to rule on broader taxes on wealth or appreciation, leaving the constitutional question open.

Conditioning market access on payment of a share tax could also face a takings challenge, especially if the stock transfer is viewed by courts as a compelled transfer of property rather than a tax payable in cash. In Horne v. Department of Agriculture (2015) the Supreme Court found a taking even where growers kept a contingent claim on the proceeds, and conditioning a government benefit on surrendering property raises an unconstitutional-conditions question of its own. Both are reasons to preserve a cash alternative.

The path to constitutionality is plausible, but a challenge is likely. If the courts ultimately classify the liquid wealth tax as a direct tax, Congress would likely need to enact a constitutional amendment, the same route it took after Pollock to enable the income tax.

The liquidity issue is likewise deferred. A covered firm does not have to raise cash or sell assets to issue new non-voting shares, so a force-selling spiral is avoided. The cash question comes later, when the public fund that receives the shares needs cash to pay a dividend or finance public spending. Much of the share-to-cash conversion could run through machinery that already exists: dividends and buybacks by the share issuers. Over 2020–2024, the largest U.S. firms returned roughly $1 trillion or more a year to shareholders through buybacks and dividends combined

Although the annual dilution is small, markets would price a permanent levy all at once, marking covered shares down today by the value of all the future dilution. The markdown would be on the order of 15 to 25% at a 1% rate, borne by whoever holds covered equity when the tax becomes a credible prospect.

The serious objection to any capital tax is that it lowers the expected return on new investments and so less gets built. But the tax would reach only firms above a high threshold, and by the time a firm arrives there, the investment that built it has already succeeded.

Another incentive distortion would occur inside the covered firms themselves. Value retained in a covered firm bears the dilution every year, while value paid out to shareholders escapes the base, so the levy leans on large firms to pay their earnings out instead of reinvesting them. This is the effect I would watch most closely.

That leaves capital flight, the hardest of the three problems. By taxing wealth through corporations rather than individuals, we can overcome capital flight by making the tax conditional on market access. While a firm can move its capital, or even its founder, it cannot move its customers.

From market access to a global club

Enforcement through market access inverts the asymmetry that doomed earlier wealth taxes. The U.S. alone accounts for nearly a third of global household consumption

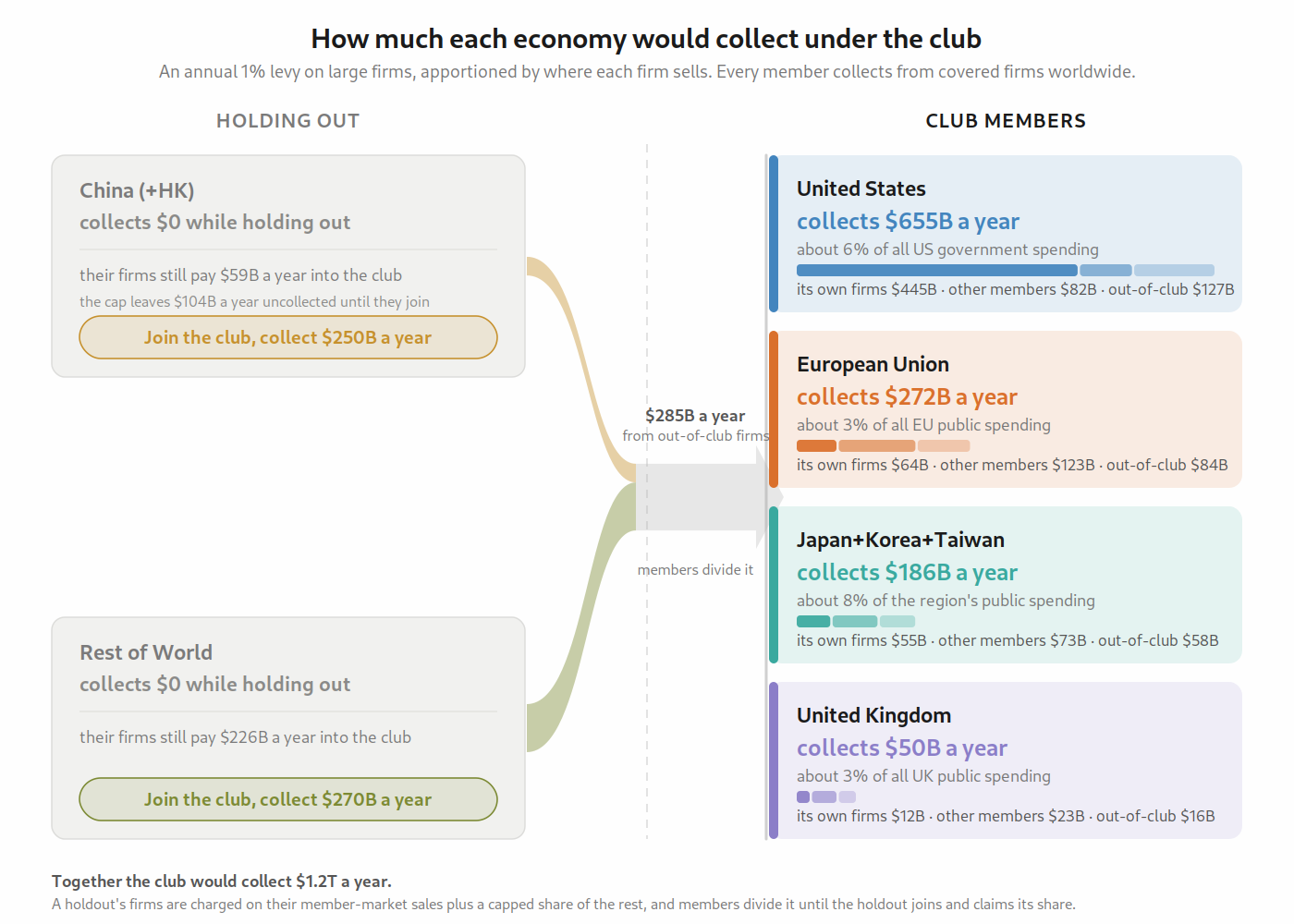

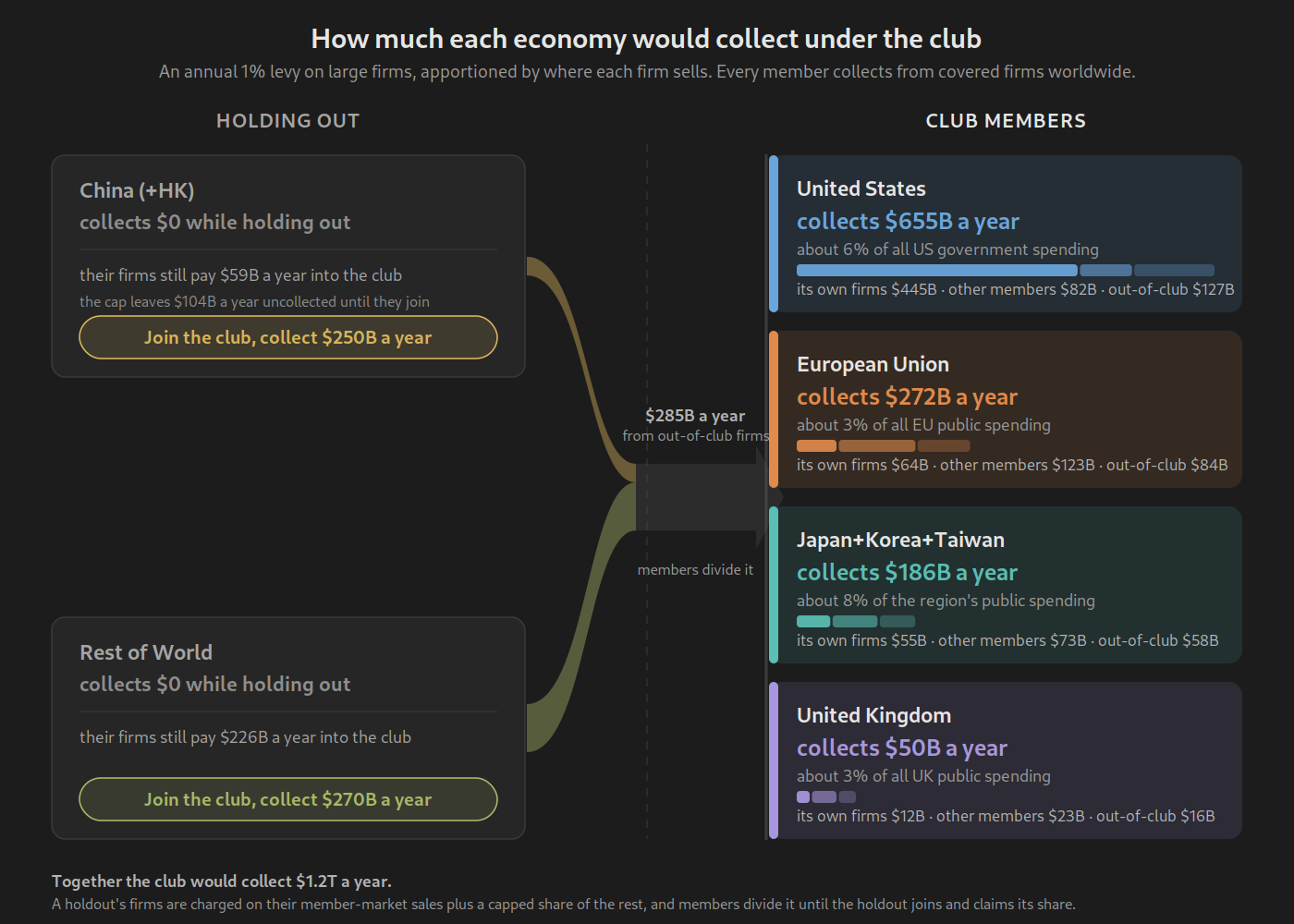

This concentration of consumption creates an opportunity for one large market, the U.S., to go first in a way that incentivizes the entire world to follow, without waiting for a treaty or a negotiated global agreement. As first mover, the U.S. would have the unilateral ability to set the amount of the tax. How it uses that power decides whether the rest of the world follows or fights. Taxing every firm that sells to Americans the maximum amount it can without having them exit the U.S. entirely, keeping all of the money, and paying only Americans would invite a trade war. The version that works is an offer, which extends to every country the same claim the first mover makes for itself. The U.S. collects the share that matches sales in the U.S., France the share that matches sales in France, and India the share that matches sales in India. A foreign company selling to Americans is treated the same as an American company selling to Americans, and an American company selling abroad is treated like any other company selling there.

Since going first is not without its costs,

Thus, a country that joins collects its share, but a country that holds back does not shield its firms from the tax. So long as those firms keep selling into the club’s markets, they must pay the share matching their home-market sales as well (up to the cap).

Click any economy to move it in or out of the club. The simulation code and the full data notes are on GitHub.

While much of the dilution would be borne by the shareholders of foreign firms, that asymmetry cuts both ways, with foreign investors holding close to a fifth of U.S. corporate equity

One asymmetry survives full membership. American portfolios hold roughly half of the world’s covered equity and would therefore bear about half of the initial worldwide markdown, while the sales matrix gives the U.S. fund about 37% of collections. In distributional terms, this makes the levy resemble a source-based tax more than a strictly domestic individual wealth tax: collections follow customer markets rather than investor residence. This asymmetry does suggest, however, that a politically viable bargain may have to give the United States more than its sales share, e.g., through a temporary founder’s credit, a modest ownership-based component, or some combination of the two.

Charging for market access is not new. A tariff does exactly that, but it raises the price of goods at the border, so much of the cost lands on the taxing country’s own consumers. Further, because it targets goods by where they come from, it invites retaliation.

A closer precedent than tariffs is a law that used U.S. market access to change the behavior of firms worldwide. In 2010, the U.S. Foreign Account Tax Compliance Act (FATCA) required essentially every bank in the world to report on its American account holders. The alternative was a 30% tax withheld from their U.S. payments. Since access to the U.S. financial system mattered more than the burden of reporting, the banks moved to comply. Where home-country secrecy laws stood in the way, intergovernmental agreements struck after the fact cleared the path.

Even if the club never forms, the United States would still collect from its own covered firms, and the dividend arithmetic in Figure 4 uses that domestic base alone. Failure would sacrifice the global reach and AI-governance extension, but the mechanism would retain its standalone value as a wealth tax.

Extending the club to AI governance

The tax gives members a continuing reason to sustain the club, and the same machinery might support a second bargain, this time over AI governance. International cooperation on AI is stuck on a familiar problem. Commitments are voluntary, and every proposal to set standards or slow down runs into the same objection, that restraint by one side hands the lead to the other. The existing tools do not answer it. Export controls and sanctions punish, but a punished state’s best answer is to build its own supply, so the stick weakens each time it is used. Voluntary commitments ask for restraint and offer goodwill in return. By contrast, by paying countries their share of the tax, club membership could be used as a direct incentive for cooperation.

To use the club for AI governance, members would impose and enforce a common set of conditions on every firm selling into the club, wherever the firm is headquartered.

How much governance the club buys depends on whether the relevant states join, and joining is binary. Market access reaches commercial deployment more readily than frontier training, military systems, or state programs that need not sell anything into the club. For a state that stays out, the club’s conditions reach only what its firms sell into member markets, and, depending on the club that forms, that may not be much. China’s frontier labs sell little into the West today (their fast-growing export revenue is, by most accounts, concentrated in Southeast Asia and the Middle East). So a club without China might buy little of the governance that matters, and the race would continue. The club’s own conditions would be written with that in mind, since members would not handicap their firms against a rival that accepted no constraints.

For a state that joins, the club offers that state’s share of the levy in exchange for its cooperation on enforcing governance on its own firms. For China, the fact that the same governance conditions would bind American frontier labs could be a substantial benefit in itself. The economic benefit also compounds with time, since the levy’s rate, as proposed below, rises with AI’s advance, so the payment for membership grows alongside the capabilities that make the race dangerous. If the payment and reciprocal restraint clear each state’s strategic bar, the members can stop racing each other and start watching each other for cheating, a different and older problem. While the club would not solve it, every member would be on the side of wanting it solved.

Coupling the wealth tax with AI governance is not without costs. Bundling gives an opponent of either piece a reason to fight both. The tax revenue arrives as soon as a country joins, while the strategic benefit of reciprocal restraint is less certain, so countries are incentivized to seek the revenue without accepting the conditions. The conditions would therefore have to be a prerequisite of joining, and a coupled club would grow more slowly than a tax-only club. Since nothing in the tax case depends on the coupling, the choice can be made after the club exists.

Public ownership without control

A public fund taking 1% of corporate equity each year raises a fear that it would slowly nationalize the economy. But even at a 1% rate, the fund would hold around 18% of covered equity after twenty years and 39% after fifty years, and these are upper bounds that assume the fund never parts with a share. In practice, buybacks by the issuing firms, occasional sales to fund the dividend, and new firms entering the market would pull the stake lower.

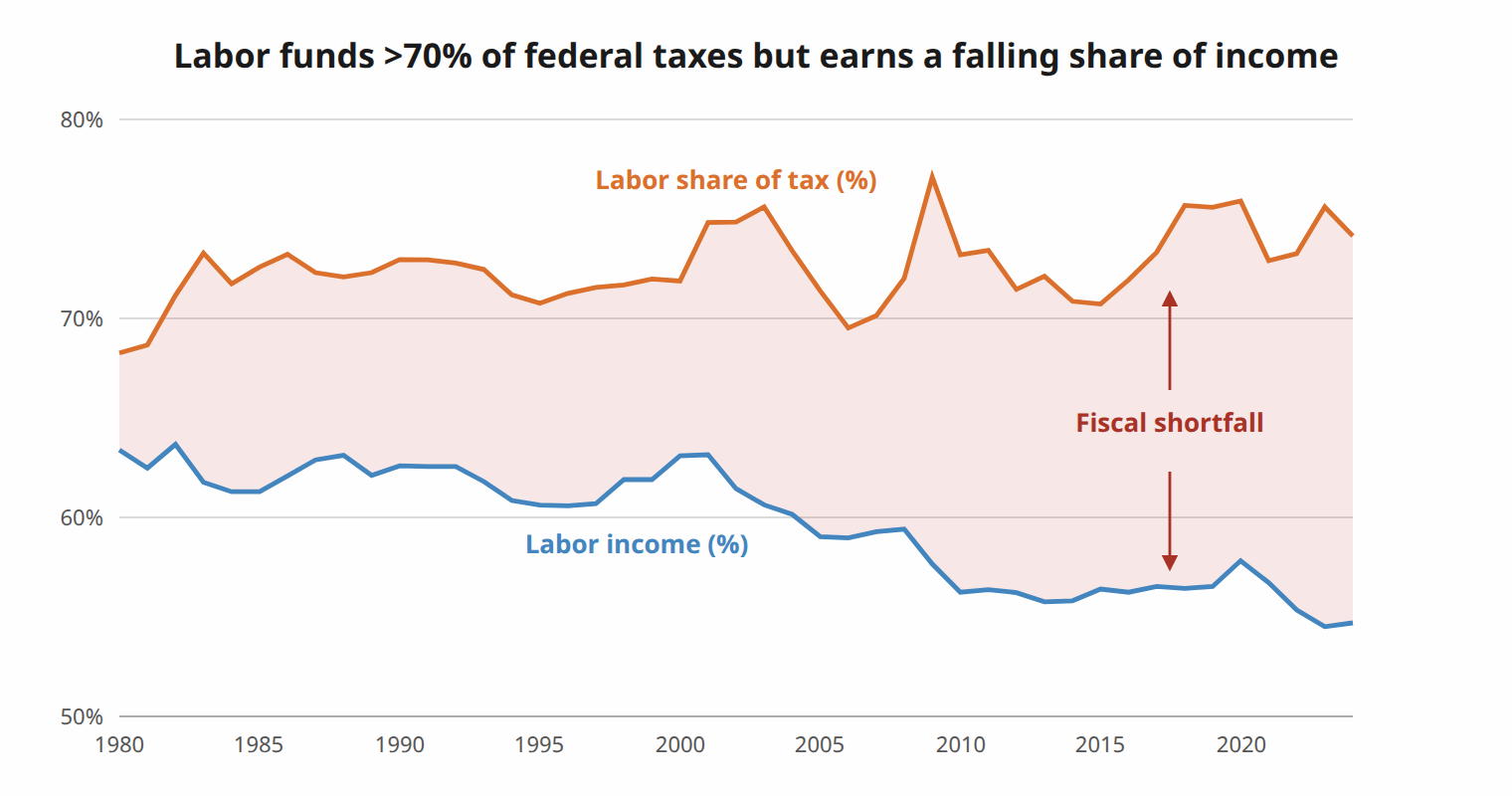

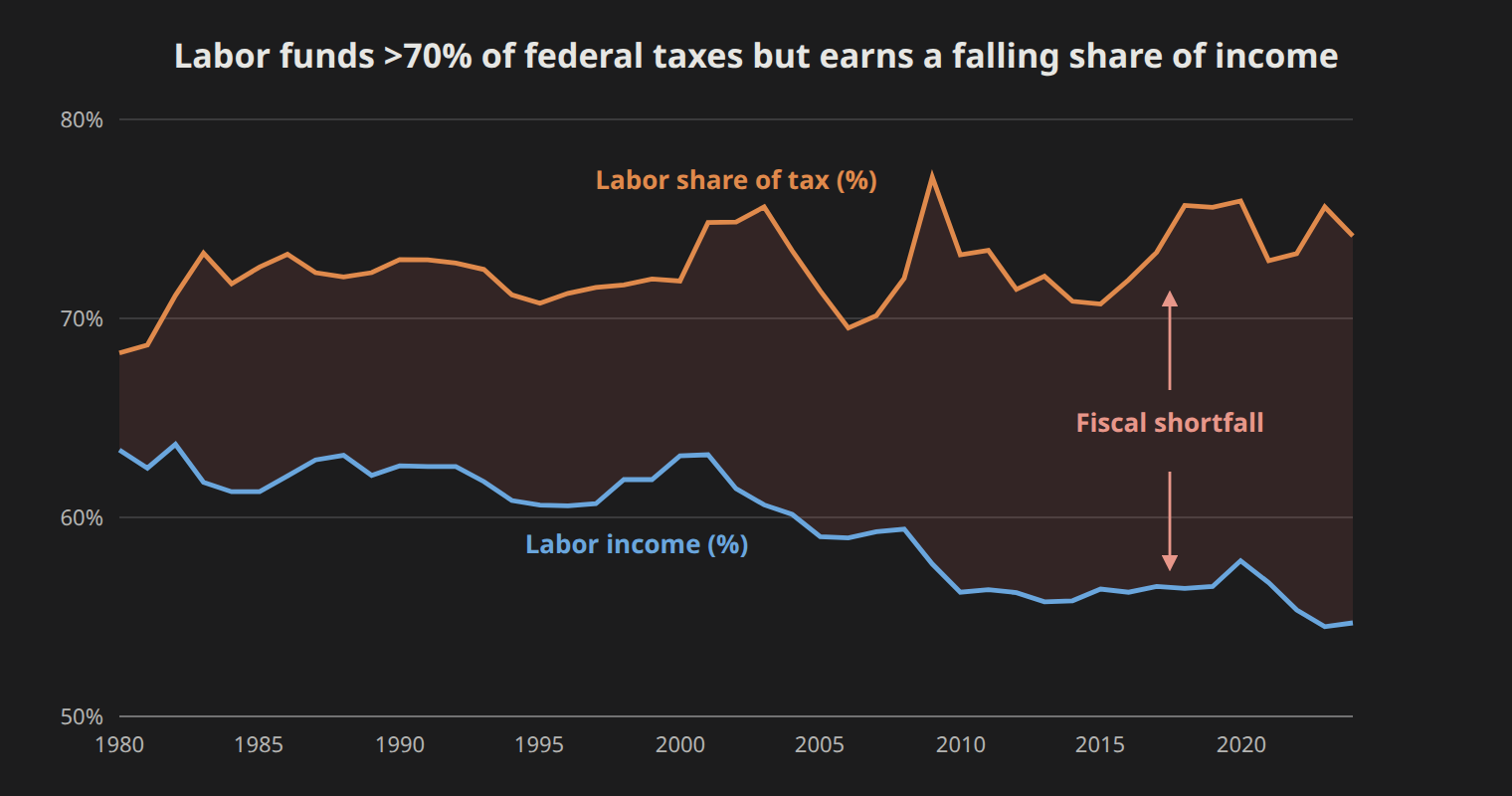

For perspective, labor currently earns around 55% of income (Figure 1). If AI shifts a large part of that income to capital, a fund holding a minority stake after decades of accumulation would claim only a fraction of the returns that used to flow to wages.

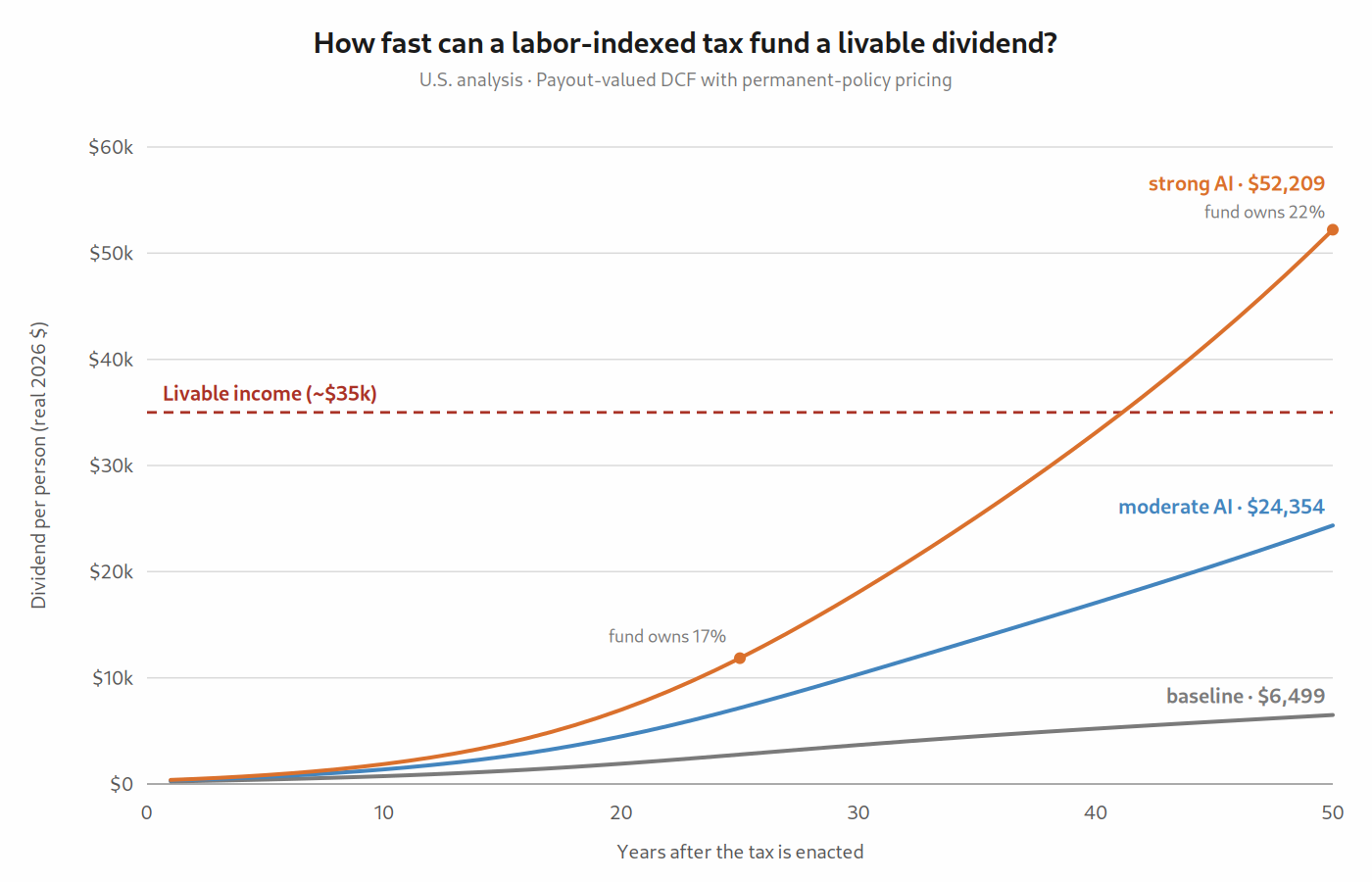

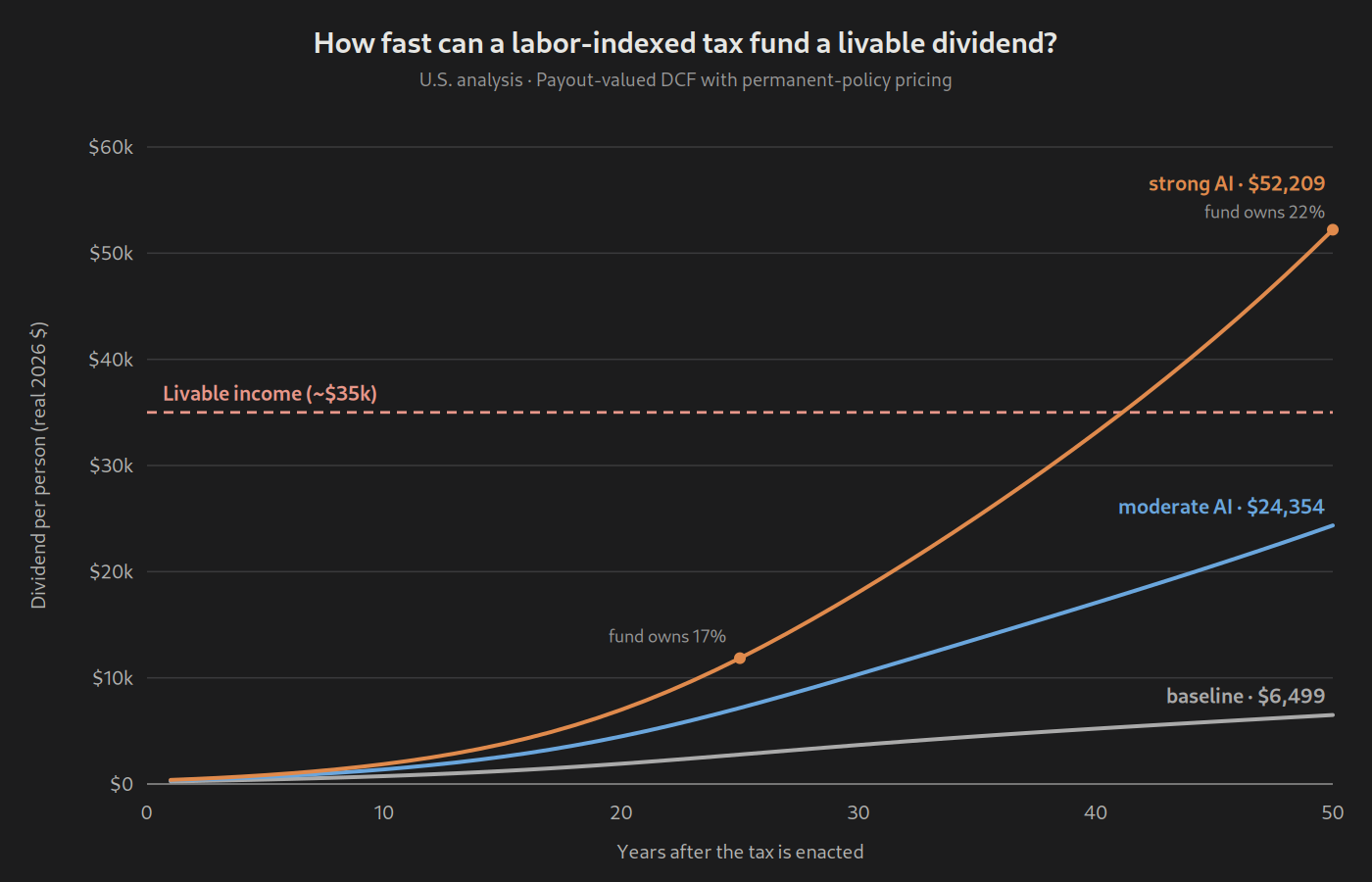

If we want to fund a sufficiently large dividend, significant public ownership cannot be avoided. Even a fund that passes much of the levy through to citizens as it arrives would come to hold a substantial share of covered equity along the way. In the simulation behind Figure 4 (below), the fund holds 14 to 22% of covered equity after fifty years, depending on the scenario.

For ownership on that scale to be politically and economically sustainable, the fund’s shares must carry no votes, and thus no direct control.

A public dividend

Early on, the fund’s accumulated holdings would start small and compound slowly, so its natural first use is insurance. As AI displaces particular workers and industries, the fund can cushion the transition, paying those most directly displaced while displacement is still identifiable

Displacement insurance has a shelf life. After enough displacement, it becomes impossible to say who was displaced. Early on you can point to the call center worker and the truck driver. But as AI diffuses into everything, we will have graduates whose entry-level job never existed, businesses that never formed because software did the work, and wages lower than they would have been. Insurance needs a victim you can name, and past some point there are no nameable victims left, just an economy producing more with less labor.

Instead, once the fund is large enough, it makes sense to pay a per-capita dividend. The dividend would be the same amount for every citizen, with no test and no claim to adjudicate. While a means test or variable dividend might still be administrable, it would give up the simplicity and the universal constituency that protects the fund politically (see Protecting the fund below). To keep the net transfer progressive, the dividend could be paid as ordinary taxable income, since the income tax claws back the most from those who need it least.

For the dividend to reach meaningful size, the fund should retain most of what it collects. Even as buybacks and dividends provide a stream of cash receipts, reinvesting that cash in the broader market allows the fund to compound while it is small. The dividend is then funded according to a preset schedule from the fund’s flows, the yield on its accumulated holdings plus a capped fraction of each year’s receipts.

Growing the dividend

How large could such a dividend get? It depends on how high the levy can go. As noted above , the levy’s cost arrives up front, through a one-time markdown of roughly 15 to 25% for a permanent 1% rate and deeper at higher rates. The market-required return on equity is the same after the markdown, so the ceiling is set partly by economics, since avoidance and distortion grow with the rate, and partly by politics, since today’s holders will not accept an excessive markdown.

Wealth holders will fight an outright loss, but parting with a share of an AI-supplied windfall is a different matter. If AI displaces enough work to move a large share of income from labor to capital, the gains to shareholders would be far larger than the markdown, so a much higher rate could go through with holders still better off than they are today. And the arithmetic is not the only consideration, since the worlds that hand shareholders the windfall are also the worlds where an economy of displaced workers puts every asset at risk.

This discussion suggests the rate should be indexed rather than fixed, rising automatically as labor’s share of income falls.

The levy already varies with outcomes in one sense. Even at a fixed percentage, its dollar value rises and falls with covered firms' market capitalization. Tying the percentage to labor's share adds a second adjustment. Shareholders give up a larger percentage when more income has shifted from labor to capital and a smaller percentage when the shift is limited. This should narrow the range of their after-tax outcomes and reduce the enactment markdown relative to a fixed levy expected to collect the same amount. The dividend provides similar insurance to households by growing most when wages fall furthest.

All other assumptions follow the essay’s assumptions footnote . The code, the model’s equations, and a plain-language walkthrough are on GitHub.

Protecting the fund

A fund this large is a standing temptation for a government short of cash. Defending it is the second reason, beyond the impossibility of singling out the displaced, to pay everyone the same dividend. Alaska’s Permanent Fund pays every resident a dividend (with no reduction in employment, though a small shift toward part-time work

But a constituency defends the fund better than it defends the rules around it. When oil revenue fell, Alaska’s governor vetoed half of the 2016 dividend’s funding, the state’s supreme court upheld the veto on the ground that the statutory formula could not bind the ordinary appropriation and veto process, and legislators have set the dividend below the formula every year since. A hundred million people who want their dividend check larger are also the coalition that would vote to raise the rate, spend down the principal, or restore the voting rights of their non-voting shares. So the voting limits and the lock on the principal need deeper entrenchment than a statutory formula. The proposed design supplies some of this on its own. The share tax collects shares of a non-voting class, so the ban on control is written into the securities themselves. And if the fund is a genuine trust whose beneficial interests vest in individual citizens, the accumulated principal might be considered their property, so a government that later reached for it may run into the Takings Clause.

Vesting creates a boundary problem of its own. The class of citizens changes through births, deaths, migration, and naturalization. Property rights strong enough to protect today's beneficiaries may also make it harder to admit tomorrow's on equal terms. The trust would need to reconcile individual vesting with a beneficiary class that changes forever.

Other proposals

While this post was being finished, versions of the idea arrived from three directions at once. OpenAI reportedly discussed giving 5% of its equity, once, to a prospective U.S. sovereign wealth fund, with Altman suggesting other leading AI firms do the same.

Each of these contains a piece of the design and omits the rest. OpenAI’s one-time 5% stake is a snapshot of today’s winners. It collects nothing from firms not yet founded, and it shrinks relative to an economy that keeps growing past it. The Sanders proposal avoids dilution from later equity issuances, but remains limited to a designated set of AI companies. The arithmetic is also not close. A one-time 5% of one firm funds a dividend of a few dollars per person per year, the Sanders fund projects about a thousand dollars a year, and even the dashed line in Figure 4, which collects 1% of all covered equity every year for fifty years, does not reach a livable income. The Sanders version also shows how an initial taking can be too aggressive while its sectoral base remains too narrow.

The instinct behind all of them is right. Anthropic writes that AI companies whose returns prove transformative have an obligation to share them broadly, and says it is ready to pay its fair share. But the gains will not stay with the companies that build the models. The leading labs are losing money today while the value shows up around them, in the chipmakers and the platforms already, and eventually in every large firm that replaces labor with software. If open models end up carrying much of the work, the builders may capture the least of it. In this way, a tax on the AI industry would miss the AI economy. This post is one attempt to specify the public’s share of that economy and the practical machinery for claiming it at the scale widespread job displacement may require.

Open design questions

Despite this post’s length, the design space is far larger than I alone can fully analyze. I’ve tried to hint at certain gaps or shortcomings in the footnotes and below, but there are likely more, and probably some errors and oversights. However, I believe the central narrative is sound, and my intent is for this proposal to serve as a starting point for discussion rather than a finished blueprint. At the very least, the following points remain underspecified by the proposal.

The levy is meant to sit alongside the corporate income tax. Swapping one for the other would raise nothing new, and the two reach value at different times. The most valuable AI companies have enormous valuations but minimal profits. For example, at OpenAI’s reported valuation, a 1% levy would require a firm that so far has no profits to tax to transfer shares worth about $8.5 billion that year. But keeping both is a significant increase in corporate taxation. At a 1% rate, the levy would collect roughly as much as the entire corporate income tax does today.

The tax base has unresolved edges. Phasing the charge in according to enterprise value softens the cliff, though firms near the band still gain from staying below it. The charge itself remains measured on equity value, which also gives firms an incentive to borrow to fund payouts and shrink the base, adding a debt bias to the incentive to distribute earnings. Private firms pose a harder valuation problem because funding rounds are infrequent and headline values can be inflated by preference terms. Coverage also has to follow size and economic function closely enough that a firm cannot escape by becoming a partnership, staying private, or delisting.

The cash payment option creates another problem. A firm that thinks its stock is overpriced will pay in shares, while one that thinks its stock is cheap will pay cash. Requiring shares would remove that choice, but the constitutional analysis above cuts the other way. The problem is worse for private firms, whose valuations are contestable, though public firms would still gain a timing advantage if the obligation were priced on a single day.

The fund’s influence over the firms it holds remains a separate risk. Non-voting shares, no board seats, and no engagement with management greatly reduce the concerns about common ownership discussed above . Residual legal rights and political pressure on managers remain, and the safeguards would have to survive decades of changing governments.

Crisis behavior is also untested. In normal times, issuer buybacks would supply much of the fund’s cash without requiring the market to absorb large stock sales. In a crisis those buybacks can stop just when the fund’s payouts are most needed. The club makes the problem larger because many national funds could sell at once. A shared rule should cap the pace of sales, route them through issuer buybacks first, and suspend them during market-wide stress.

The enforcement rule has an aggressive edge of its own. While the club is incomplete, the residual lets members collect part of an out-of-club firm’s charge on sales into other countries that have not joined. This reach makes holding out costly, but it also stretches the destination principle beyond the member markets supplying the enforcement power. Governments outside the club may retaliate against it. The grace-period escrow softens the claim by holding those shares for the absent countries, at the cost of delaying part of the reward for going first. Its treatment under the WTO and investment treaties would still require separate analysis, especially where the club reaches value attributable to sales outside its markets.

The hardest problem is the politics of a loss taken now for gains that arrive over decades. Past wealth taxes lost support after capital fled, valuations were contested, and revenue disappointed. This design tries to avoid those failures, but the repricing would still arrive when the tax becomes credible and the dividend would still take decades to matter. Indexing helps because the higher rates arrive in the futures where shareholders receive the largest gains, and holders in those scenarios can remain wealthier after the repricing than they are today.

Without explicit protection, retirement accounts would bear part of the initial loss. To remedy this, part of each firm’s levy issuance could be routed to recognized retirement funds, leaving total issuance unchanged and netting out their dilution. Limiting the offset to holdings that exist at enactment closes the obvious loophole and lets the protection run off as those savings are drawn down. Figure 4 uses this grandfathered design.

Further design questions appear in the footnotes, including the constitutional path for the levy , the division of collections among member countries , financing transition support before the fund matures , the legal definition of the labor-share index , and the durability of the trust as its beneficiary class changes .

Closing

AI threatens to move income from labor to capital faster than any technology before it. Perhaps the best response is to give citizens a direct and durable claim on the capital whose returns are replacing their wages. To do this, the cleanest instrument is a levy on large firms, paid in their own non-voting shares, enforced through market access, with the proceeds returned to every citizen as an owner’s dividend. Current capital owners have their own stake in the outcome. Asset values rest on the stability of the institutions that enforce them, and an economy where citizens own nothing is not one where property stays secure for long. Part of what the levy buys, for the owners who pay it, is the durability of the arrangement that makes their assets worth anything at all.

The United States is in a unique position, with the market power to implement such a levy and the leverage to bring the rest of the world along. The same global club could give international AI rules an enforcement mechanism and a continuing incentive for cooperation. Both possibilities should be given serious consideration now, before the transition to an AI workforce accelerates. Figure 4 shows why the work must begin early: even the ambitious path takes nearly twenty-five years to pay an annual five-figure dividend per person. But while first dividends would be small, the fund’s holdings would compound from the day it was created. And waiting compounds too, as every year without a public claim is a year the private one grows.

FAQs

Isn't this all AI hype?

The policy proposal has merit even if we froze AI's capabilities today. Labor's share has already fallen, equity is already concentrated, and the tax system already leans heavily on wages. The 1% floor is meant to address the economy we already have, and indexing the tax to labor's share of income adjusts it if the shift toward capital continues (see Growing the dividend above ).

Won't firms just raise prices and pass the cost to consumers?

Unlike a tariff, issuing shares does not directly increase the marginal cost of making or selling another unit, so the levy creates no immediate reason to raise prices. A firm that could already increase its profits by raising prices would presumably have done so. The immediate cost would therefore fall mainly on capital owners, through the markdown in the value of existing shares . Over time, however, the recurring levy could alter investment, financing, market entry, and corporate structure in ways that eventually affect prices and wages. The clearest distortion may be the incentive to distribute earnings that would otherwise be reinvested, which is discussed under A liquid wealth tax above.

Could companies escape by relocating?

Changing a company's legal home would not escape the levy because the charge follows the corporate group's sales into member markets. A covered firm could avoid it only by abandoning those customers, and for a firm with material American sales, that would generally cost much more than moving its headquarters. The possibility of withdrawal still places a practical limit on how far a country or a small club can reach (see From market access to a global club above).

Isn't this confiscation?

The levy's real cost is a markdown of covered share prices, on the order of 15 to 25% at a permanent 1% rate, relative to the value those shares would have had without the levy. Existing holders keep their shares but own a smaller fraction of the firm after it issues new stock, using the same mechanism firms already use to compensate executives and finance acquisitions. In the scenarios that drive the indexed rate higher, a holder who bears the full repricing still ends up far wealthier than they are today because the deeper markdown arrives only when AI has produced much larger gains (see Open design questions above ).

Is the levy constitutional?

The answer is unsettled because courts have never considered a levy of this form. The strongest path would be to structure it as a corporate excise tied to the privilege of doing business, with a cash payment option that reduces the risk that issuing shares would be treated as a compelled transfer of property, but a court that classified the levy as a direct tax on property could make a constitutional amendment necessary. The legal case and its limits are discussed above .

Isn't this nationalization?

The design gives the public an economic stake while withholding the powers that would let the fund direct the firms it holds. After fifty years in the strong-AI path of Figure 4, the fund owns about 22% of covered equity, but its shares carry no votes and the formal channels that could turn it into an industrial-policy board are closed (see Public ownership without control above ). In this important respect, the arrangement resembles the corporate income tax, which already gives the government a claim on part of every firm's profits without giving it control of the firm.

Why would this fare better than earlier wealth taxes?

This design is built around the valuation, liquidity, and capital-flight problems that led many European wealth taxes to be repealed (see A liquid wealth tax above). Publicly traded firms have observable market prices, payment in shares allows the firm to satisfy the charge without raising cash, and enforcement through customer markets makes a change of domicile ineffective. Private firms and the eventual conversion of the fund's holdings into cash still present difficult edges, but the central case no longer requires the government to value every asset a wealthy person owns or to prevent that person from moving abroad.

Would the levy reduce investment and innovation?

It probably would at the margin, although the size of the effect is uncertain because the levy would begin at 1%, phase in across a high threshold on the order of a billion dollars, and reach firms only after the investment that built them had already succeeded. Founders and early investors still price expected exits, so some reduction in new company formation could remain, although the higher rates would arrive in futures where AI had already multiplied the value of successful firms (see Growing the dividend above). Within covered firms, the more immediate concern is whether the levy encourages managers to distribute earnings that they would otherwise reinvest, a distortion discussed under A liquid wealth tax above.

Won't competition pass AI's gains to consumers, leaving nothing to tax?

If competition passes most of AI's gains to consumers, covered equity values will grow less and the levy will collect less. If wages also hold up, the indexed rate will remain near its floor, leaving little need for the larger public claim modeled in the stronger scenarios. The levy becomes more consequential as gains accumulate in equity values and labor's share falls, with the indexed rate rising only as far as those changes actually occur.

Why not just raise income taxes, or add a VAT?

Higher taxes on corporate profits, realized capital gains, and consumption could all supply revenue, and a VAT may well be part of the fiscal answer . Taxes on income and gains reach value only after it appears as taxable income or an investor realizes a gain, which leaves room for profits to be booked elsewhere and gains to be deferred. A VAT reaches capital income when it is eventually spent, but places a relatively heavy burden on households that consume most of what they earn. None of these policies gives citizens an ownership claim on the capital producing the income, which is the additional distributive purpose of the share levy.

Why not just tax AI companies directly?

AI's gains are unlikely to remain inside the sector that builds the models, because retailers, banks, manufacturers, and other firms will capture some of the value when they use the technology. Restricting the base to AI companies would miss those gains and invite a continuing fight over which firms qualify, especially if open models allow the builders to capture less value than their users (see Other proposals above). A size threshold reaches large firms across the economy, while indexing adjusts the rate according to the shift in labor's share that the policy is meant to address (see Growing the dividend above).

What about wealth the levy never touches, like real estate?

The levy reaches large incorporated firms, leaving wealth in real estate, small businesses, art, and other uncovered assets outside it. Much of the wealth at the very top would still be reached, since the top 1% of households hold roughly half of all corporate equities and the largest fortunes consist mainly of stakes in large companies. Extending the levy downward would reintroduce the annual valuation problems that the share-payment mechanism avoids, while housing would remain the sharpest gap because land and rent absorb a large share of any livable budget. Land and housing policy would therefore be a natural companion to this design.

Won't retirees and pension savers bear the cost?

Without protection, retirees and pension savers would bear part of the initial markdown. Figure 4 therefore protects savings already held in recognized retirement accounts when the levy is enacted by routing enough of each firm's new shares to those accounts to offset their dilution, while the public fund receives the balance. This slows the public fund's growth, but the protection phases out as the grandfathered savings are withdrawn, and new contributions need no offset because they buy shares at prices that already reflect the levy .

Could a future government raid the fund?

No ordinary statute can remove that risk permanently, because one Congress can revise the work of an earlier one. The proposed trust would vest beneficial interests in individual citizens, and the fund's non-voting shares would carry their limits inside the securities themselves, making both the principal and the ban on corporate control harder to reach. These protections would create legal and political barriers rather than an absolute lock, and the unresolved problem of preserving them as the beneficiary population changes is discussed above .

Won't other countries retaliate?

Other countries may retaliate, especially while the club is small and the first mover is collecting shares whose ultimate owners live abroad. The design limits that risk by treating domestic and foreign firms alike and offering every country the same right to collect on sales into its own market, so a government that fought the system would also be declining revenue available to it through membership (see From market access to a global club above). Retaliation could still place serious pressure on the founder's own firms during the period between the levy's becoming credible and the club's becoming large, and the precedents and limits are discussed in the footnotes there , .

Would American investors bear more than the United States collects?

Under full membership, the current estimates say yes, because American portfolios hold roughly half of the world's covered equity and would bear about half of the initial worldwide markdown, while the sales matrix gives the American fund about 37% of collections. Some asymmetry is consistent with ordinary source-based taxation, under which countries tax economic activity within their markets rather than matching receipts to the residence of investors. It still creates a real negotiating problem for the first mover, and a temporary credit funded from the residual shares collected while the club remains partial could narrow the gap without changing the market-access rule or permanently directing most collections toward the countries that already own the most capital .

Why pay everyone instead of only the people actually displaced?

Payments can remain targeted so long as particular workers and industries can still be identified as displaced, which is why the design begins with insurance for those directly affected. As AI diffuses across the economy, the causal line between one person's job loss and a particular system will become harder to draw even if the aggregate wage share continues to fall, and a narrowly administered program would miss much of that broader loss (see A public dividend above). A universal dividend extends compensation across the economy-wide shift and creates the broad constituency that would help protect the fund over time (see Protecting the fund above).

Isn't the dividend too small to matter?

The dividend would be far too small to replace lost wages during its early years, so workers displaced before the fund matures would need separately financed transition support . That delay strengthens the case for beginning early, since even the ambitious indexed path needs nearly twenty-five years to reach an annual five-figure dividend per person (Figure 4). A recurring levy also keeps acquiring shares in firms that become valuable later, allowing the public's claim to grow with the economy instead of leaving it with a one-time stake in today's winners (see Other proposals above).

What will people do without work?

Nothing in this proposal answers that question, which remains important because work supplies structure, identity, and community along with income, while a dividend replaces the income alone. If AI ends work as the default organizer of adult life, people will need other sources of purpose, such as hobbies, sports, and learning, along with communities and social institutions that organize those pursuits as schools, professions, and workplaces once did. A tax design cannot build those institutions, although the dividend could provide the material security people need while they search for purpose and community elsewhere.